STATE OF OPTICAL

INDUSTRY INTEL

A look at The Vision Council’s report and recent research on the state of optical

At Vision Expo West in Las Vegas, Shawn Shafer, program manager at The Vision Council, presented the group’s state of the industry to attendees. As its exclusive media partner for this report, here we offer a glimpse at some of the Council’s findings.

In terms of overall economic trending, consumers remain in the dark about how the Affordable Care Act may impact their vision care. Approximately 34% of adults surveyed say they simply don’t know, while only around 8% report they plan to decrease spending on eyewear and eyecare as a result of the ACA.

RETAIL SALES

On a very positive note, Shafer reports that over the last three years, retail sales have increased in all categories except refractive surgery (which shows a drop of 7%).

Comparing the year ending June 2012 to the 12 months ending June 2014, The Vision Council reports:

Contact lenses…+11.6%

Spectacle lenses…+10.7%

Sunglasses…+9.4%

OTC readers…+8.3%

Eye exams…+5.5%

Frames…+4.7%

| MALE | FEMALE | |

|---|---|---|

| U.S. Population | 48.7% | 51.3% |

| Rx Wearers | 45.8% | 54.2% |

Source: The Vision Council

FRAME UNIT PURCHASES: By Material - 6ME June 2014

Source: The Vision Council

CATEGORY GROWTH

As for market share by business format, the percent of eye exams conducted by independents has continued to steadily increase over the last four years—up from 66.9% in 2011 to 68.7% through June of this year.

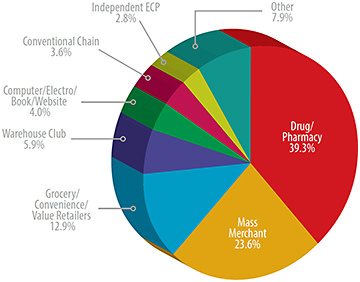

One area where the independent lags way behind other channels, however, is in over-the-counter readers. In fact, only 2.8% of consumers surveyed report they bought readers from an independent ECP during the 12 months ending in June. The big winners in this category continue to be drugstores, which are responsible for just under four out of every 10 pairs of readers sold, and mass merchants, which retain nearly a quarter (24%) of reader sales.

BUYING TRENDS

How ECPs buy continues to change, as participants in the most recent Buying Group survey, conducted in August, report that 78.2% of frame purchases were made through a purchasing or IPA group. As for future intent, nearly three out of 10 ECPs report they will purchase more of their product from their buying group going forward.

Wherever they buy, ECPs find that business is strongly affected by weather. For the first quarter of 2014, weather did, in fact, have a huge impact on sales up and down the East Coast.

That impact was certainly reflected in the number of eye exams by region for the quarter. While the number of exams rose nearly 5% for the six-month period ending March 31 in most regions of the country, the Northeast and Southeast saw much lower increases—of just over 1%—due to inclement weather.

LENS PRICES

Regardless of weather, geographic location, or mode of delivery, the average retail selling price paid for prescription lenses continues to increase. According to consumers surveyed, the average price paid for a pair of lenses was $144.44 for the 12 months ending this June. That is up $4 a pair from an average of $140.16 a year earlier.

THE GENERATIONS

| AGE GROUP | 18-34 | 35-44 | 45-54 | 55+ |

|---|---|---|---|---|

| U.S. Population | 30.5% | 17.8% | 18.0% | 33.7% |

| Rx Wearers | 25.0% | 15.0% | 19.1% | 40.9% |

Source: The Vision Council

Consumers also report paying the most per pair of Rx lenses from independents and the least from mass merchants and clubs. The difference is sizeable.

The average price from an independent, as reported by consumers, is $165.45 for the 12 months ending in June vs. $151.94 from a conventional chain, $132.71 in a department store optical, and just $84.62 at a mass merchant or club location.

OTC READERS UNIT SALES BY CHANNEL: 12ME June 2014

Source: The Vision Council

KEY CATEGORIES

Here’s a look at lenses by percent of pairs sold in several key categories for the 12-month period ending in June 2014:

Photochromics…15.7%

Rx Sun…7.0%

AR…29.5%

PALs…29.5%

All PAL price points have not seen the same growth, however. The high end is seeing the biggest upswing, with 45.4% of PAL sales coming from premium, high-end product (with an average sale price of $331 per pair). Growing fastest, however, are digitally surfaced, free-form PALs, which already lay claim to 28.7% of the progressive lens market, at an average sale price of $332.

SUN OR SNOW?

According to Steve Kodey, senior director of industry research services, climate will continue to impact eyewear sales. “Many economic experts are predicting that difficult winter sales seasons may continue over the decade as the world deals with…global climate change.

“On the other hand,” adds Kodey, “we are expecting a solid sunglass season…as the hurricane forecast suggests [few] storms will make landfall. Better weather will have a beneficial impact on eyewear sales.”

FRAME FACTS

Independents continue to expand their share of the market, with frame sales up 2.8% among independent ECPs from mid-2013 to June of this year. On the other hand, a big drop—of 3.2% in dollar sales—was seen in department store frame sales during that same period.

Metal frames continue to dominate the market, with all-metal frames representing 36.8% of units sold during the six months ending June 30, followed by combination plastic and metal eyewear coming it at 28.4%, plastic at just under 20%, and rimless/semi-rimless at just under 9% of units sold.

EXAM INTENT: Percent of Adult Population Likely to Get an Exam Within the Next Three Months

Source: The Vision Council

ONLINE SALES

While online retail sales remain small as a share of the total market, dollars spent online have nonetheless risen in the two years since June 2012.

Online contact lens sales have only increased 16.5% over that period, while plano sunglasses have jumped 35.5%, spectacle lenses 31.3%, and frames 27.2%.

Looking ahead, consumers who have purchased eyewear through traditional channels in the last six months vary in their likelihood to purchase eyewear “with the assistance of” the Internet in the future. Only 14% of consumers who had recently bought from an independent ECP say they “may” buy a complete pair of glasses online, while 21% of those who recently bought from chains said they’d consider purchasing “with the assistance of the Internet” in the future.

REPURCHASE CYCLES

While most of the results presented by The Vision Council represent good news for the marketplace, purchasing frequency stats aren’t so cheery. In fact, the time between buys, currently pegged at 2.2 years, varies greatly depending on both the demographics and age of wearers. Consumers between the ages of 35 and 44 buy on average every 1.9 years, while Americans over 55—who need vision correction most—only buy new glasses every 2.6 years.

The repurchase cycle also varies by income. Consumers in households whose income is under $60,000 a year buy less frequently—once every 2.6 years. Adults in more affluent households, where the income is over $60,000, report buying eyewear much more frequently—every 1.9 years.

FUTURE FOCUS

Looking ahead, Shafer indicates that the gradual see-saw recovery in the U.S. economy will generate optimism for the rest of this year as well as 2015. He points to the upward trending of leading economic indicators as well as rising consumer and business confidence.

In terms of optical-specific trending, he adds that purchase intent is still relatively high and that the demographics of “likely” buyers are returning to pre-recessionary patterns. The best news? The Vision Council points to ECPs becoming more optimistic about the future.